Navigating the Impending Merger: Comprehensive Insights into the Combined R&D Tax Relief Schemes

The recent Autumn Statement officially announced the merger of the R&D tax relief schemes, scheduled to take effect from 1st April 2024, for accounting periods starting after this date. This significant reform, following a consultation opened in January 2023 and subsequent policy papers, particularly impacts companies engaged in Research and Development (R&D) activities.

The supporting documentation, released shortly after the Autumn Statement, outlines the groundwork for combining the Small and Medium Enterprise (SME) and Research and Development Expenditure Credit (RDEC) schemes. This impending merger, affecting all claiming companies, prompted our comprehensive analysis of the associated rules.

Confirmed in the Autumn Statement on 22nd November, the merger will follow RDEC rules, highlighting the role of R&D in a company’s pre-tax income. Larger businesses accustomed to the RDEC scheme’s ‘above-the-line credit’ approach may experience a smoother transition, while SMEs are advised to proactively plan for the impending changes.

Key Components of the Merged Scheme:

1. Definition of R&D: The fundamental DSIT Guidelines, remains unaltered, requiring companies to demonstrate uncertainties and advancements in science or technology.

2. Rates of Relief: A proposed unified relief rate of 20%, resulting in a net benefit of 15% or 16.2% depending on corporation tax rate for companies Large and Small.

3. A specialised relief rate scheme for SME R&D-intensive companies (net benefit of 27%) will persist alongside the merged scheme. Though after March 2024 the definition of a research-intensive company will drop from R&D spend at 40% to 30%, adding an anticipated 5,000 eligible companies to this scheme.

4. SME PAYE Loss Cap Rules: The more favourable SME scheme PAYE loss cap rules are slated for adoption, with the notional tax rate applied to loss-making companies set at 19%.

5. Subcontracted R&D: The scheme permits broader claims on outsourced R&D costs for the R&D decision maker, akin to the current SME scheme, though details on contract terms that specify this are still being consulted on.

6. Subsidised R&D: Unlike the current SME scheme, subsidised expenditure rules won’t apply to the new merged scheme, ensuring that relief remains unaffected if a company receives a grant for R&D costs.

Already announced:

In the earlier spring statement and previous announcements, the Government had already added in maths and cloud–computing costs as eligible and that overseas sub-contractor costs would become ineligible unless the R&D has to take place abroad for geographical, social or legal reasons.

Impact on Businesses:

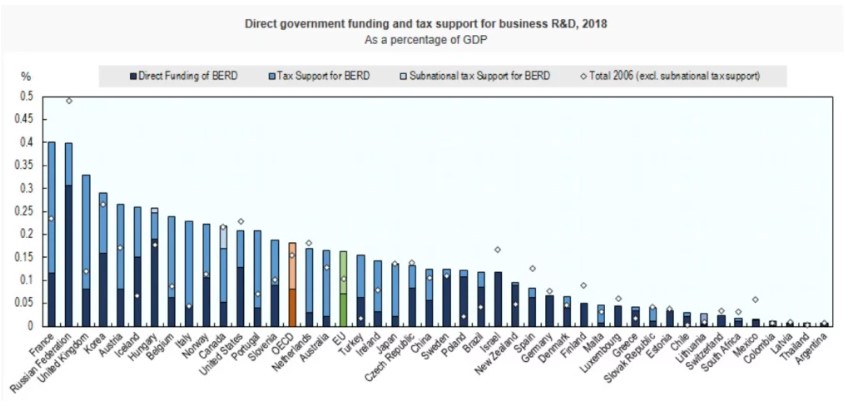

The merger has broad implications for companies involved in R&D activities, potentially reducing benefits for smaller enterprises. Noteworthy changes to rules on R&D decision makers, subsidised R&D and overseas costs necessitate careful planning, especially for businesses receiving grants or contracts for sub-contracted R&D. The increased benefit rate for the RDEC scheme to 15-16% is a significant boost for Large Companies but will this be competitive enough among international schemes where some countries offer the following benefit:

France 40%

Korea 28%

Austria 26%

United States 22%

UK 15-16%

For the SME in the UK the benefit has dropped from 25-33% to 15-27%, a significant hit and again does this make the UK an attractive place to carry out R&D, especially when HMRC are being quite aggressive in challenging R&D claims made by SMEs.

How to prepare:

Contrary to expectations of a potential one-year delay, the Autumn Statement confirmed the merger’s timely implementation. Businesses, especially SMEs, are urged to be proactive in readiness for potential changes. We welcome inquiries for advice, offering assistance in evaluating impacts, resource sourcing, contract terms and recommending necessary organisational adjustments.

Government’s Objectives:

The government’s objective is to make the UK a world leader in R&D as a driver of innovation and economic growth. The merged scheme aligns with their goal of tax simplification and prudent use of taxpayers’ money.

Graph source – New data on R&D Tax Incentives from OECD

Article written by: Ian Davie, Senior Consultant – TBAT Innovation Ltd

To discuss how we may be able to assist with your R&D Tax Claim, or if you have any queries, please contact Jo Rudzki, confirming you are an STC Member jor@tbat.co.uk or visit www.tbat.co.uk for further information

Author: TBAT Innovation

Date: 22 July 2024

The R&D Tax Relief Scheme is, in essence, a form of non-competitive government funding delivered through the taxation system. It offers significant financial incentives to businesses spending money on eligible R&D activities. Understanding who can claim and what activities qualify for R&D tax can often be quite complex. This blog aims to shed some light on these … Continued

Author: TBAT Innovation

Date: 22 July 2024

Thursday 26th September 10:00am – 11:00am ONLINE Join TBAT Innovation for this insightful webinar with our expert Ian Davie, Senior Consultant, where he will delve into the dynamic landscape of R&D Tax Credits. In this free 1-hour webinar, you will discover the latest updates, key strategies , and expert insights to maximise your returns. Whether … Continued

Author: TBAT Innovation

Date: 27 June 2024

Could you be our Winner? The 2024 Innovation Challenge is powered by TBAT Innovation with headline spoonsor Shakespeare Martineau. We’re excited to announce that the application window is now open! Who can apply for the Innovation Challenge? – Start-ups: UK Businesses three years old or younger – Aspiring Entrepreneurs: Those seeking to launch a business … Continued